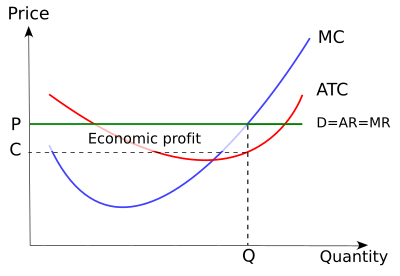

45 if the competitive firm depicted in this diagram produces output q, it will

2. the equilibrium position of a competitive firm in the long run. 3. a competitive firm that is realizing an economic profit. 4. the loss-minimizing position of a competitive firm in the short run. 9. Refer to the above diagram. If this competitive firm produces output Q, it will: 1. suffer an economic loss. 2. earn a normal profit. Figure 13 - 14 illustrates a monopolistically competitive firm. 7) Refer to Figure 13 -14. Which of the following statements describes the firm depicted in the diagram? 7) A) The firm is making no economic profit and will exit the industry. B) The firm is in long - run equilibrium and is breaking even.

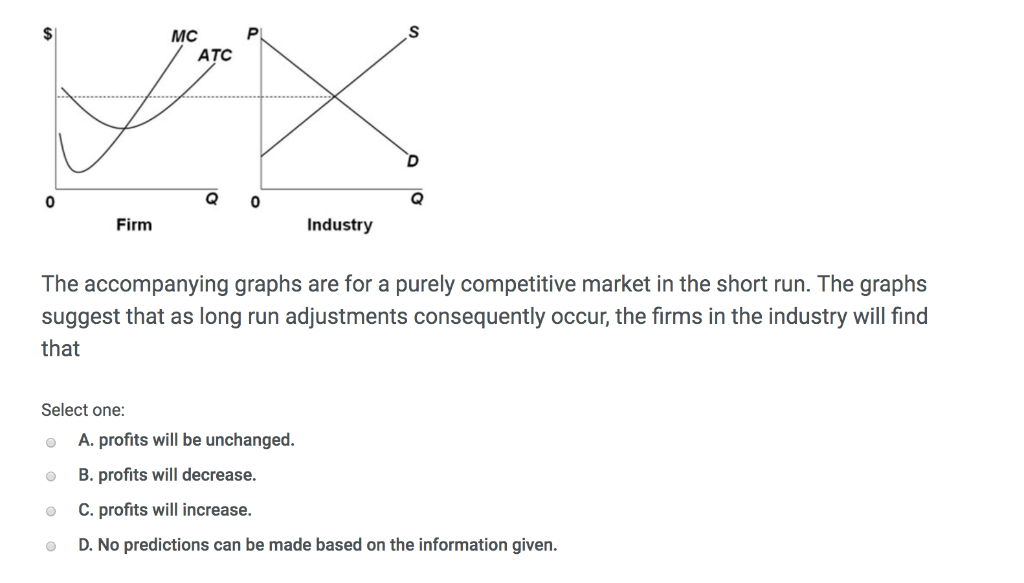

if 100 units can be produced for $100, then 150 can be produced for $150, 200 for $200, and so forth. ... which pertain to a purely competitive firm producing output q and the industry in which it operates. The predicted long-run adjustments in this industry might be offset by ... Refer to the diagram. At output level Q2, answer choices

If the competitive firm depicted in this diagram produces output q, it will

A firm produces output using capital and labor. The firm's marginal product of labor (MPL ) is 5050 and its marginal product of capital (MPK ) is 20. Suppose the wage per unit of labor (w) is $6.00 and the cost per unit of capital (r) is $3.00. where Q is total output, i.e. Q = Q 1 + Q 2. a. On a diagram, draw the marginal cost curves for the two factories, the average and marginal revenue curves, and the total marginal cost curve (i.e., the marginal cost of producing Q = Q 1 + Q 2). Indicate the profit-maximizing output for each factory, total output, and price. Since revenue (OP B E B Q B) for OQ B output is the same as that of its cost of production (OP B E B Q B), Firm B enjoys only normal profit. Point E B may be called break-even point since revenue equals cost. Firm C incurs a loss though it attains equilibrium at point E C. In other words, a competitive firm may reach equilibrium even after ...

If the competitive firm depicted in this diagram produces output q, it will. 13) All firms in a competitive industry have the following long-run total cost curve: C(q) = q3 - 10q2 + 36q where q is the output of the firm. a. Compute the long run equilibrium price. What does the long-run supply curve look like if this is a constant cost industry? Explain. b. Refer to the above diagram. If this competitive firm produces output Q, it will: a. suffer an economic loss. b. earn a normal profit. c. earn an economic profit. d. achieve productive efficiency, but not allocative efficiency. (Supposed to be a graph) If the competitive firm depicted in this diagram produces output Q, it will a.) suffer an economic loss. b.) earn a normal profit. c.) earn an economic profit. d.) achieve productive efficiency but not allocative efficiency. competitive output and input markets uIn perfectly competitive industries, ... a profit maximizing firm produces where P=MC. ... use of "q" for the firm' s output, and "Q" for the market P P q/t Q/t D S Firm Market p 1 p 1. Profit Maximization in the Short Run up 1 is the firm' s

The following TWO questions refer to the diagram below, which illustrates the demand, marginal revenue, and relevant cost curves for a monopolistically competitive firm. 1. How many units of output should this firm produce, in order to maximize profits? a) 10. b) 25. c) 30. d) 60. 2. In the long run, what price will this firm charge for its ... In the competitive firm, the firm sets… View the full answer Transcribed image text : 6 MC ATC Price MR 00:45:49 Q, Q Quantity If the competitive firm depicted in this diagram produces output Q, it will Multiple Choice suffer an economic loss. achieve productive efficiency but not allocative efficiency. earn an economic profit. If the competitive firm depicted in this diagram produces output Q, it will. earn a normal profit. Marginal cost is _____. (TVC+TFC)/Q. The diagram shows the average total cost curve for a purely competitive firm. At the long-run equilibrium level of output, this firm's total revenue ... Refer to the provided graph for a purely competitive firm ... Suppose a production function is given by Q=min(L,K). So inputs are perfect complements. Draw a graph of the demand curve for labor when the firm wants to produce 10 units of output (Q=10) DO not u...

If the competitive firm depicted in this diagram produces output Q, it will earn a normal profit. Technological advance improves productivity in a purely competitive industry. This change will result in a shift down of the individual firm's MC curve, causing the market (industry) supply curve to shift to the right. Professional academic writers. Our global writing staff includes experienced ENL & ESL academic writers in a variety of disciplines. This lets us find the most appropriate writer for any type of assignment. The rule for a profit-maximizing perfectly competitive firm is to produce the level of output where Price= MR = MC, so the raspberry farmer will produce a quantity of approximately 85, which is labeled as E' in (a). Remember that the area of a rectangle is equal to its base multiplied by its height. 26) Refer to Figure 9-1. The diagram shows cost curves for a perfectly competitive firm. If the market price is P1, the profit-maximizing firm in the short run should A) produce output A. B) produce output B. C) produce output C. D) produce output D or shut down as it doesnʹt really matter which.

In Step 1, the monopoly chooses the profit-maximizing level of output Q 1, by choosing the quantity where MR = MC. In Step 2, the monopoly decides how much to charge for output level Q 1 by drawing a line straight up from Q 1 to point R on its perceived demand curve. Thus, the monopoly will charge a price (P 1 ).

If the industry depicted in this graph were purely competitive, then the market price would be -$25, which is lower than what the price would have been if the industry were a monopoly. 47. Refer to the diagram for a monopolistically competitive firm. Long-run equilibrium output will be -D. 48.

summation of each firm's output at each price. 800 40 Q P S 6. Suppose that a competitive firm's marginal cost of producing output q is given by MC(q) = 3 + 2q. Assume that the market price of the firm's product is $9: a. What level of output will the firm produce? To maximize profits, the firm should set marginal revenue equal to ...

Mar 01, 2012 · Over the period we examine, we find firm-level TFP growth of manufacturing firms averaging 2.85% for a gross output production function and 7.96% for a value added production function. Total TFP growth for the manufacturing sector was even higher due to massive entry of new firms with above average productivity levels and growth rates and the ...

(4.4 Page 407) The graph represents the situation of a perfectly competitive firm. Indicate on the graph the areas that represent the following: a. Total cost=ATC*Q b. Total revenue=P*Q c. Variable cost=AVC*Q d. Profit or loss=(P-ATC)*Q Briefly explain whether the firm will continue to produce in the short run.

View Homework Help - ECONHW12Sols19.pdf from ECOP 1003 at The University of Sydney. 60. Award: 1.00 point If the competitive rm depicted in this diagram produces output Q, it will suffer an economic

produces the quantity of output at which marginal cost equals price, since for the perfectly competitive firm price equals marginal revenue. A perfectly competitive firm can produce its current level of output at an average total cost of $10 and a marginal cost of $8.

If the competitive firm depicted in this diagram produces output Q, it will suffer an economic loss. earn a normal profit. earn an economic profit. achieve productive efficiency but not allocative efficiency. earn a normal profit. If the industry depicted in this graph were a pure monopoly, the product price would be lower than $8. $8. $14. $16.

54. Refer to the above diagram. If this competitive firm produces output Q, it will: A. suffer an economic loss.B.earn a normal profit. C. earn an economic profit.D. achieve productive efficiency, but not allocative efficiency. 55.

Again, the perfectly competitive firm will choose the level of output where Price = MR = MC, but in this case, the quantity produced will be 75. At this price and output level, where the marginal cost curve is crossing the average cost curve, the price the firm receives is exactly equal to its average cost of production.

B) Each type of firm produces a homogeneous product. C) In the long run, firms in both industries make zero economic profit. D) Each type of firm competes on product quality and price. Answer: C . 32) Excess capacity is the . A) difference between a perfectly competitive firm's and a monopolistically competitive firm's output.

A supply curve, tells us how much output it will produce at every possible price. We have seen that competitive firms will increase output to the point at which P = MC, but they will shut down if P < AVC. Thus, for positive output the firm's supply curve is the portion of the MC curve that lies above the AVC curve.

The rule for a profit-maximizing perfectly competitive firm is to produce the level of output where Price= MR = MC, so the raspberry farmer will produce a quantity of 90, which is labeled as e in Figure 4 (a). Remember that the area of a rectangle is equal to its base multiplied by its height.

If the above competitive firm produces a quantity exceeding qo, then MR and Po would be less than MC, the firm would incur an economic loss on the marginal unit, so the firm could increase its profits by decreasing its output until it reaches qo. If the above competitive firm produces a quantity fewer than qo, then MR and Po would be greater ...

Taking first‐order conditions with respect to output q, yields and rearranging yields p=MC(q). Perfectly Competitive Markets From our above profit maximization problem of firms operating in a perfectly competitive industry, we concluded that each of them increases their output q until p=MC(q).

The following diagram shows a typical firm's short-run output in a competitive market. In the long run the industry's output will decrease and the typical firm's output will: Able Pads, Inc., sells plain white printer paper in a perfectly competitive market.

A company has the following cost information, where Q is output and TC is total cost: Say the firm is a monopoly. If the firm will maximize its profit when marginal revenue equals $25, at what outp...

Since revenue (OP B E B Q B) for OQ B output is the same as that of its cost of production (OP B E B Q B), Firm B enjoys only normal profit. Point E B may be called break-even point since revenue equals cost. Firm C incurs a loss though it attains equilibrium at point E C. In other words, a competitive firm may reach equilibrium even after ...

where Q is total output, i.e. Q = Q 1 + Q 2. a. On a diagram, draw the marginal cost curves for the two factories, the average and marginal revenue curves, and the total marginal cost curve (i.e., the marginal cost of producing Q = Q 1 + Q 2). Indicate the profit-maximizing output for each factory, total output, and price.

A firm produces output using capital and labor. The firm's marginal product of labor (MPL ) is 5050 and its marginal product of capital (MPK ) is 20. Suppose the wage per unit of labor (w) is $6.00 and the cost per unit of capital (r) is $3.00.

0 Response to "45 if the competitive firm depicted in this diagram produces output q, it will"

Post a Comment